The rise of Argentine mining

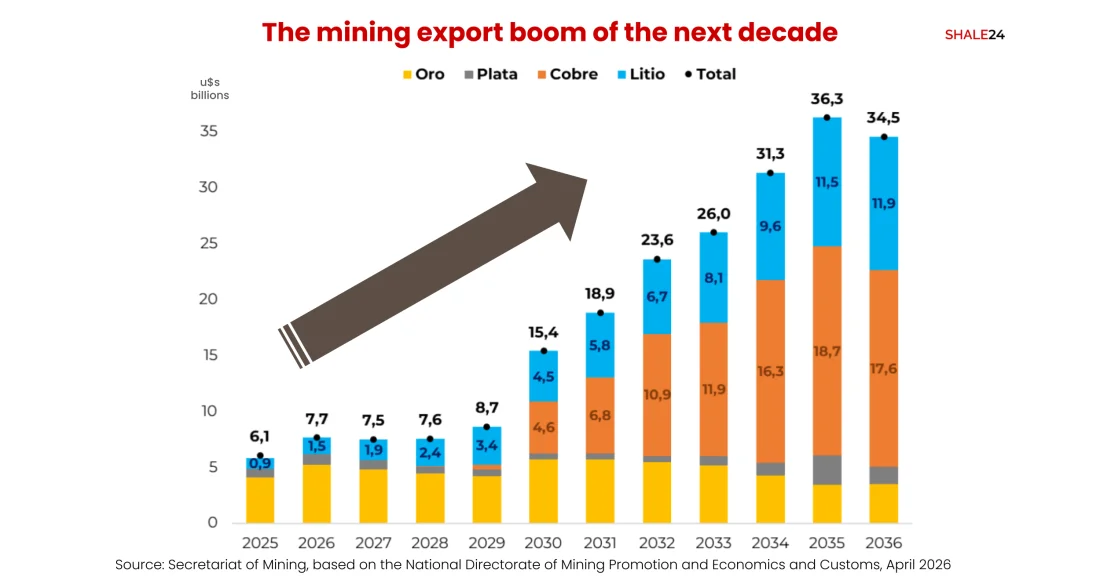

Argentina's National Mining Secretariat projects the country's mining exports will multiply nearly sixfold by 2035 to $36.25 billion, from the $6.1 billion record posted in 2025. Delivering the curve requires a minimum capex floor of roughly $57 billion, concentrated in copper and lithium.

The projection, prepared by the National Directorate of Mining Promotion and Economy, anticipates an exponential growth curve over the coming decade. The 2025 record, achieved in a year when mining has historically run well behind agricultural exports as a source of foreign currency, marks a threshold rather than a ceiling, driven by rising global demand for the strategic minerals required by electromobility and new technology supply chains.

Whether the curve holds will depend on factors the projections cannot yet resolve, among them the speed of environmental permitting in the copper provinces of San Juan, Mendoza and Catamarca, the financing structures that convert headline project commitments into drawn capex, and the durability of Argentina's Large Investment Incentive Regime (RIGI) across investment cycles that in copper routinely extend a decade or more.

The trajectory moves to $7.66 billion this year, $15.4 billion by 2030, and peaks at $36.25 billion in 2035.

A Reconfiguration of Argentina's Export Base

At the mid-decade mark, mining export revenues would run at close to six times the 2025 figure. The reconfiguration moves Argentina away from a near-exclusive dependence on the agricultural sector, historically the country's largest foreign currency earner, and toward a matrix in which energy and mining take progressively larger shares.

Copper and Lithium Displace Gold and Silver

Copper is the headline variable. After recording marginal exports of just $13 million in 2025, the red metal is projected to climb to $4.62 billion by 2030 and to consolidate at $18.71 billion by 2035, accounting for more than 50% of Argentina's total mining exports.

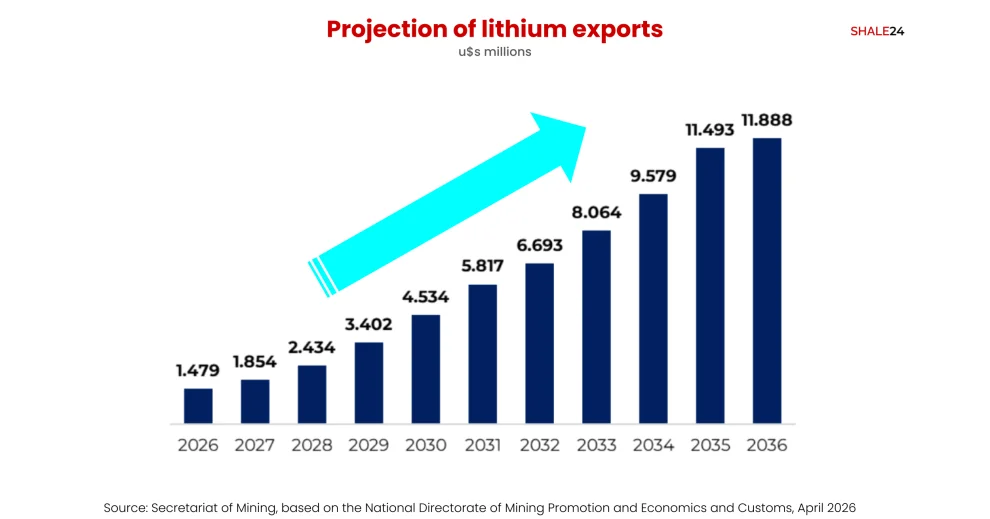

Lithium follows a parallel trajectory, moving from $911 million exported in 2025 to $4.53 billion projected for 2030 and reaching $11.89 billion by 2036.

As critical minerals for modern technology gain ground, the traditional leaders of Argentine mining enter a maturation cycle with gradual declines in direct export volumes. Gold, which held the top position in 2025 with exports of $4.09 billion, is expected to stay relatively stable through 2030 at $5.7 billion. From the following decade onward, the projections show gold exports easing as several deposits approach end of life, dropping to $3.45 billion by 2035 and into third place behind the new leaders.

Silver follows a similar curve, declining from $785 million exported in 2025 before stabilizing and then staging a recovery to $2.6 billion by 2035 — a rebound driven primarily by the by-product output the large copper projects contribute once they enter operation.

Attracting High-Quality Foreign Direct Investment

Turning the projections into tangible output on the ground demands a substantial capitalization effort, opening opportunities for attracting high-quality foreign direct investment.

The pipeline of mining projects will require a minimum capex floor of roughly $57 billion to enter operation and deliver the projected export flows. The distribution of that capital mirrors market priorities. Of the $57 billion total, $41.19 billion is concentrated in the large-scale development of nine copper projects, followed by $14.05 billion for the expansion and construction of twelve lithium operations across the country.

Up to 80% of Value Retained Domestically

Beyond the impact on the trade balance, the domestic business ecosystem and the real economy are expected to capture the multiplier effect characteristic of modern extractive activity.

Of the projected $36.25 billion in 2035 mining exports, government estimates suggest that between 67% and 80% of the gross production value could remain and be reinvested within Argentine borders, translating into a direct injection into the domestic economy of between $24.29 billion and $31.61 billion.

Those funds would be channeled primarily into building out the local value chain associated with mining activity: pull-through for small firms and provincial suppliers, high-skill technical wages, social security contributions, and fiscal collection via profits tax, production tax, and royalties paid to the producing provinces. In Argentina, subsurface resource ownership rests with the provinces rather than the federal government, and royalties flow to the producing province directly — a distinction that is material for investors evaluating provincial versus federal sovereign risk.

The Argentine mining horizon is taking shape as a new pillar for long-term economic and industrial development.