Large Investment Incentive Regime

When the Large Investment Incentive Regime (RIGI) — a flagship investment framework introduced by Argentina’s government to attract large-scale capital — took effect in October 2024, the energy sector set the pace. The first three projects approved were a solar park in Mendoza, an oil pipeline linking the Vaca Muerta shale formation to the Atlantic coast and a floating gas liquefaction plant in the Gulf of San Matías. The message was clear: the regime was designed as a tool to unlock the infrastructure needed by the Vaca Muerta boom. Seventeen months later, mining has flipped the equation.

With the approval on Feb. 27 of the expansion of Veladero — the country’s largest gold mine, operated by Barrick Mining and Shandong Gold in San Juan — and the Diablillos project — a gold and silver deposit developed by Canada’s Abra Silver in the provinces of Salta and Catamarca — the mining sector now accounts for six of the 12 projects authorized under the regime.

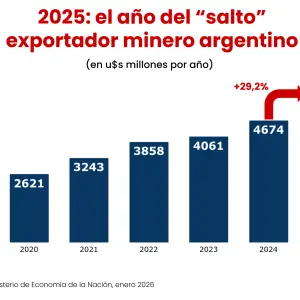

Altogether, the 12 approved projects represent more than $26 billion in investment commitments, according to Argentina’s Ministry of Economy. Within that total, mining accounts for the bulk of the capital committed under the program.

Energy dominated the early months

In practice, the first year of RIGI was dominated by hydrocarbons and related infrastructure.

The Vaca Muerta Oil Sur pipeline — backed by YPF alongside Pan American Energy, Vista, Pampa Energía, Pluspetrol, Chevron and Shell, with an investment of $2.486 billion — and Southern Energy’s floating liquefied natural gas (FLNG) project — a $6.878 billion plan to install a liquefaction barge in the province of Río Negro — were the two largest projects approved during that initial phase.

Mining took longer to get started. Its evaluation process is structurally more complex, involving environmental impact studies in high-altitude regions, interprovincial agreements and feasibility timelines measured in years rather than months.

“The delay is linked to the structure of the RIGI approval process, which involves 16 secretariats and subsecretariats,” Roberto Cacciola, president of the Argentine Chamber of Mining Companies, said in mid-2025.

How mining took the lead

The turning point came in May 2025, when the government approved the first mining project under the regime: Rincón, Rio Tinto’s lithium development in Salta, with an investment of $2.724 billion.

Approvals accelerated from there. In the following months, additional projects were cleared, including Hombre Muerto Oeste — a $217 million lithium project by Galán Lithium in Catamarca — Los Azules — McEwen Copper’s $2.672 billion copper project in San Juan — and Gualcamayo, a $665 million gold project also located in that Andean province.

The two approvals announced on Feb. 27 complete that cycle. Veladero will receive $380 million to expand its leach pad and add 1.6 million ounces of additional production, extending the mine’s life to 2034 and generating projected exports of $3.8 billion over the life of the project.

Diablillos, by contrast, is a new mine. Abra Silver will build the operation from scratch, developing a deposit with measured resources of 186 million ounces of silver and 1.6 million ounces of gold. It will become the first silver mine to enter production in the province of Salta.

Together, the two projects are expected to generate more than 2,300 direct and indirect jobs in San Juan, Salta and Catamarca, with exports estimated at about $750 million annually, according to the Ministry of Economy.

The map of the 12 approved projects

Geographically, the distribution shows a notable concentration along the Andes corridor. San Juan has the largest number of approvals, with three mining projects totaling $3.727 billion — Los Azules, Gualcamayo and Veladero.

It is followed by Salta — with the Rincón project and the Salta portion of Diablillos — and the Neuquén–Río Negro corridor, where the major energy projects are anchored.

By sector, energy still holds the lead in total approved investment — in terms of capital authorized — largely due to the scale of Southern Energy’s FLNG project. However, in the number of projects and in the size of the pending pipeline of proposals, mining clearly leads.

The pipeline ahead: copper as the next chapter

Projects currently under evaluation suggest the gap could widen further. The most significant case is Glencore, which has submitted requests totaling $13.5 billion for two copper projects: El Pachón in San Juan — one of the largest undeveloped copper deposits in the world, containing copper, molybdenum and silver resources in the San Juan Andes — and MARA in Catamarca, which will reuse infrastructure from the historic Alumbrera mine. The Swiss mining company expects RIGI approval for El Pachón in the first half of 2026 and plans to start construction in 2029, with first production targeted for 2034.

At the same time, Vicuña Corp. has submitted Josemaría and Filo del Sol projects totaling $18 billion. If both are approved, RIGI will have catalyzed within just over two years a mining project pipeline that Argentina has not seen in decades.

In February, the government expanded the regime to include upstream oil and gas projects with a minimum investment threshold of $600 million. The signal is that energy is not giving up ground.

For now, however, the momentum belongs to mining.