Hormuz risk is priced into Brent

As long as Hormuz risk is priced into Brent, Argentina's distance from global markets, long a Vaca Muerta penalty, increasingly works as a strategic asset rather than a handicap.

Around 20 million bbl/d of crude normally transits the Strait of Hormuz, roughly a fifth of global oil consumption. Each time tensions rise in the Persian Gulf, the market embeds a risk premium: not because flows are necessarily about to disappear, but because they could. That conditional is enough to move prices. Argentine crude leaving the Atlantic via Puerto Rosales, Argentina's primary Atlantic crude export terminal in Buenos Aires province, navigates none of these chokepoints: neither Hormuz, nor the Suez Canal, nor Bab el-Mandeb, the maritime chokepoint connecting the Red Sea to the Gulf of Aden.

Whether that contingent advantage translates into durable repricing for Vaca Muerta, one of the world's largest shale plays in Argentina's Neuquén Basin, will depend on factors the market cannot yet resolve: how long Hormuz risk remains priced into Brent, the pace of bypass investment by Persian Gulf producers, and the regulatory and infrastructure execution that determines how much Vaca Muerta crude actually reaches the Atlantic. What can be said now is narrower: in a market that has put chokepoint risk back at the center of oil pricing, physical reliability of delivery carries weight alongside reserves and breakeven costs.

Bypass Capacity Has Always Fallen Short of Hormuz Volumes

The producer response to Hormuz exposure is decades old, with partial results.

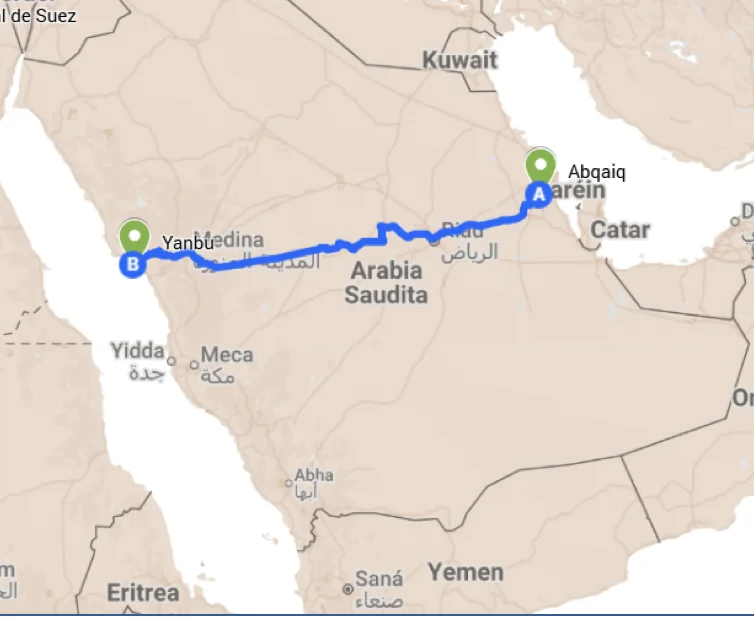

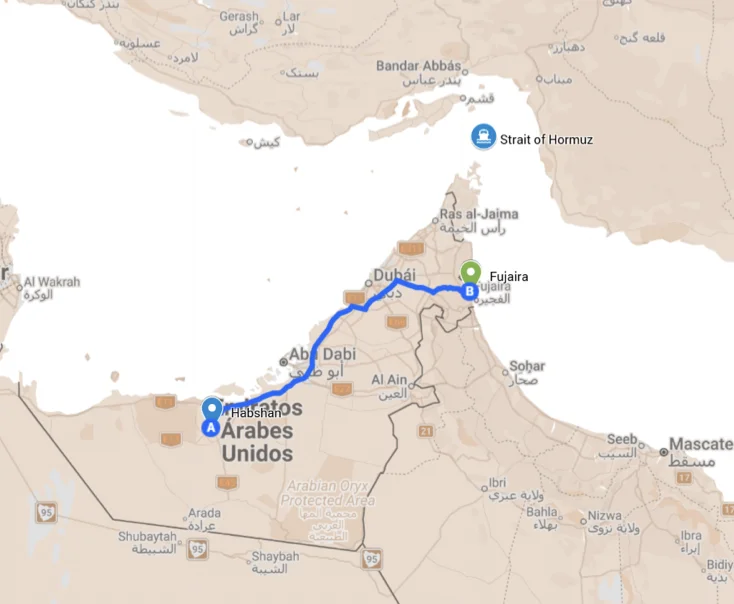

Saudi Arabia built the Petroline system, also known as the East-West Pipeline, in the 1980s, connecting its eastern oilfields to the Red Sea coast at Yanbu and explicitly designed as insurance against Persian Gulf disruption. Capacity: roughly 7 million bbl/d. The United Arab Emirates followed decades later with the Abu Dhabi Crude Oil Pipeline (ADCOP), moving crude from Habshan to Fujairah outside the Persian Gulf, with operational capacity of about 1.5 million bbl/d (rising to 1.8 million bbl/d at maximum). Even combined, these alternative routes cover at best one-third of normal Hormuz throughput. The remainder still depends on the strait.

Eilat-Ashkelon: A Tactical Tool, Not a Structural Solution

A smaller piece of the bypass architecture, historically and logistically interesting, is the Eilat-Ashkelon pipeline.

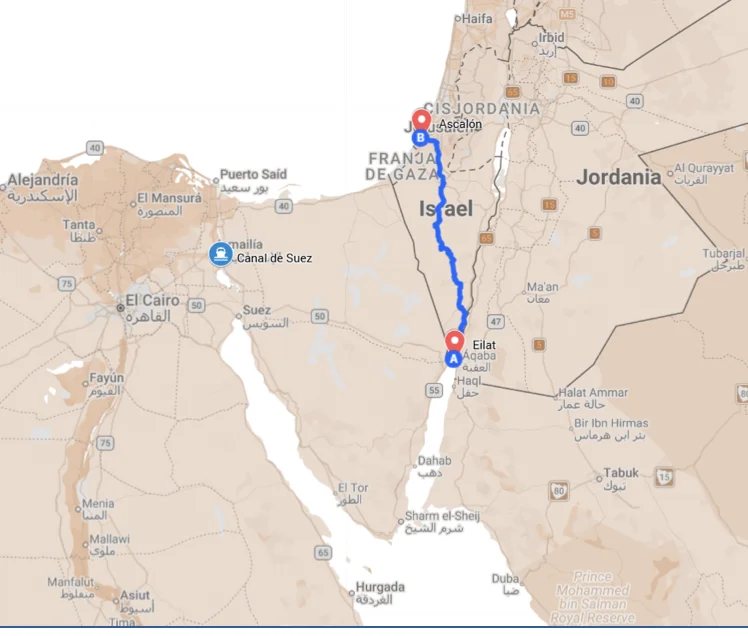

It was not built in response to Hormuz. It emerged from a different crisis: the closure of the Suez Canal after the 1967 Six-Day War. In the late 1960s, Israel and Iran (then under Shah Mohammad Reza Pahlavi) jointly developed the line as a way to move Iranian crude to Europe without depending on Suez. The pipeline received crude at Eilat on the Red Sea, transported it overland, and re-exported it from Ashkelon on the Mediterranean.

The 1979 Iranian Revolution broke the arrangement. Bilateral relations collapsed, and the pipeline became entangled in legal disputes that lasted decades, with Israel maintaining operations through a state-owned entity while Iran demanded compensation and an equity stake.

Over time, Eilat-Ashkelon has found new uses. Rather than serving a fixed origin-to-destination flow, it now functions as a flexible piece in global logistics, capable of running in reverse and moving crude from Ashkelon to Eilat when market conditions warrant. Its capacity is limited: roughly 1.2 million bbl/d northbound (Eilat to Ashkelon, the original Red Sea-to-Mediterranean direction) and 400,000 bbl/d southbound (the reverse-flow direction enabled by a 2003 retrofit). In a system that moves tens of millions of barrels daily, that makes it a tactical instrument, not a structural fix. Its use is also politically conditioned (not all producers can or will route crude through Israeli infrastructure) and constrained by environmental concerns, particularly in the Red Sea ecosystem.

A point often overlooked: to reach Eilat, Persian Gulf crude must already have transited, directly or indirectly, the Strait of Hormuz. The pipeline does not avoid the system's primary chokepoint. It avoids a different one. It is a second-order bypass.

This is the common feature of all such projects. None eliminate the underlying problem. They fragment it and make it more manageable. They do not resolve it.

Bypasses Fragment the Problem; They Don't Solve It

The global energy system continues to depend on a small number of strangulation points where geography and geopolitics overlap. Hormuz, Suez, and Bab el-Mandeb are not places where supply and demand meet freely; they meet under conditions of friction. That friction can be reduced through investment in pipelines, terminals, and storage, but the geography itself cannot be negotiated away. It can be circumvented, buffered, or managed, but not eliminated.

Each time one of these points enters the risk window, the market embeds a premium. The mechanism is not that flows are certain to be interrupted, but that they could be. That conditional is what moves price.

Argentina's Position Outside the Funnel

On that global map, one anomaly is relevant for Argentina: Vaca Muerta. Not for its scale, but for its location.

Argentina sits far from the major demand centers, far from the most heavily trafficked routes, and far from the historic trading hubs. For decades, that distance translated into a disadvantage: more freight, more time, more associated cost. But in a world where risk concentrates at specific geographic points, that same distance begins to work in Argentina's favor.

A barrel leaving Puerto Rosales toward the Atlantic does not need to cross a militarized strait or navigate corridors where multiple strategic tensions converge. The route is, by comparison, more direct and more predictable. That does not make Argentina immune. Oil prices remain global, and any Hormuz disruption registers everywhere. But it introduces a meaningful difference: lower exposure to extreme physical interruptions. In high-tension scenarios where Persian Gulf flows are threatened, delivery reliability gains relative weight. Reserves and competitive costs are not enough; the capacity to reliably deliver the barrel matters too. That is where geography starts to show up in pricing.

The Argentine paradox is clear. The country sits far from demand, but also far from the principal current geopolitical risks. That double condition implies costs in normal times and potential benefits in periods of stress. The advantage is not linear. It is contingent. But in a market that reacts abruptly to any signal of disruption, that contingency can become central.

The world will continue to invest in infrastructure to reduce dependence on these chokepoints, with more bypasses, more capacity, more redundancy. But chokepoints are unlikely to disappear entirely. The geographic concentration of supply, combined with the distribution of demand, ensures that some critical point always exists. The system can become more resilient but never fully secure. In that imperfect equilibrium, assets like Vaca Muerta occupy a particular place: not because they are better positioned in every scenario, but because they are positioned differently.

In energy, as in maps, what matters is not always being closer. Sometimes it is being outside the funnel.

Gustavo Araujo is Head of Research at Criteria, an Argentine investment management and research firm.