Records and challenges

In a year that will go down as a turning point for Argentine shale, the country’s oil and gas sector doubled its drilling pace, from 538 wells completed through December 2024 to 1,075 a year later.

That is according to the monthly statistical report from Oil Production Consulting, which recorded 631 productive wells completed in 2025 alone, including 54 in December: 46 oil and eight gas.

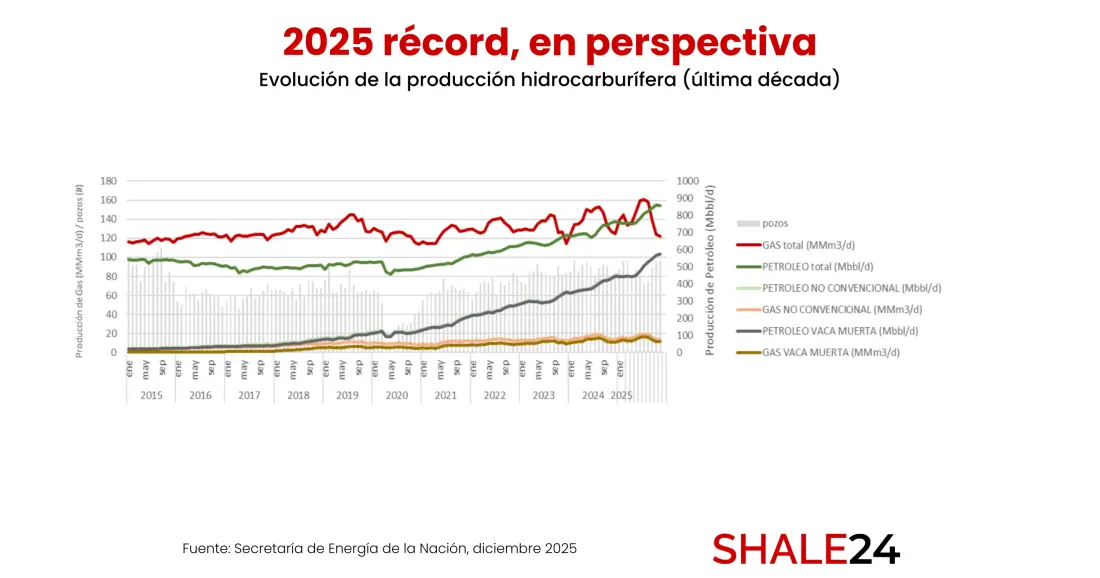

This explosive 100% increase not only offset the relentless natural decline rates in shale, which can reach up to 80% in the first two years, but also propelled production to record levels: oil rose 15% year-on-year to 138,118 m³/day, with 68% coming from unconventional sources, while gas remained stable at 131,529 Mm³/day thanks to conventional production offsetting a 20% decline in shale output.

The phenomenon goes beyond mere statistics. It represents a deep reconfiguration of Argentina’s energy map, with the Neuquén Basin accounting for 76% of drilling activity (478 wells completed) and a convoy of operators led by YPF, Pan American Energy (PAE) and Vista Energy, supported by contractors such as Nabors Industries and San Antonio Internacional.

But what triggered this boom amid falling Brent prices and operating costs roughly 40% higher than in the United States?

The answer lies in a strategic combination of record investments totaling $11.2 billion, fiscal incentives like the RIGI, technological efficiency gains, and key export agreements.

Structural drivers of the boom

The growth was neither spontaneous nor improvised. First, record investments set the pace for the sector: YPF led with $4.589 billion invested in 2025 and projected $6 billion for 2026, a 20% increase. PAE invested $1.417 billion, Vista $1.178 billion, and Pampa Energía contributed as well.

Collectively, these investments — totaling over $11.2 billion, with 63% concentrated in unconventional Neuquén — were largely financed through the Régimen de Incentivos para Grandes Inversiones (RIGI), which offers 30-year fiscal stability for projects over $200 million, attracting majors such as Chevron and Shell.

Second, the operational efficiency revolution reshaped the landscape. Established techniques such as pad drilling — which allows 20 to 40 wells to be drilled from a single platform, reducing logistical costs by 15% to 20% — and extended horizontal “superwells” dramatically increased productivity per unit.

A paradigmatic example is La Amarga Chica operated by YPF, which already outperforms Loma Campana, the flagship Argentine shale block since 2013. Standardized automated hydraulic fracturing adds to this, with projections of 28,000 stages in 2026, up 22% from 2025.

Third, export-driven infrastructure secured the investment-production cycle. The Vaca Muerta Oil Sur (VMOS) project will enable the direct export of 230,000 barrels per day of crude from the Neuquén Basin, while the Gasoducto Perito Moreno will add 35 MMm³/day of capacity to neighboring countries.

Seven major operators — YPF, PAE, Vista, Pampa, Chevron, Pluspetrol and Shell — committed $3 billion collectively to pipelines and terminals, securing premium markets for Argentine shale.

Finally, regulated domestic prices — despite Brent volatility — incentivized prioritization of shale oil over associated gas, explaining impressive monthly peaks: 57 wells completed in June, 52 in July and 49 in August, compared with seasonal winter declines (33 in January, 31 in May). December 2025 closed with 54 wells, consolidating momentum toward 2026.

Top 10 operators: YPF dominates with 44%

Production rankings — the best proxy for drilling intensity — illustrate concentration of power.

- YPF leads with 61,114 m³/day (44.3% of national total), anchored in Loma Campana, Bandurria Sur and La Amarga Chica in Neuquén.

- PAE follows with 16,815 m³/day (12.2%), balancing Neuquén shale (Lindero Atravesado) with its conventional stronghold at Cerro Dragón in the San Jorge Gulf Basin.

- Vista Energy contributes 11,073 m³/day (8%) from Bajada del Palo Oeste/Este, Pluspetrol 6,315 m³/day from La Calera and Bajo del Choique–La Invernada, and Shell 5,370 m³/day via Cruz de Lorena and Sierras Blancas.

The remaining operators include Chevron with 3,631 m³/day at El Trapial Este, Pampa Energía 3,397 m³/day at Rincón de Aranda, Petrolera El Trébol 2,962 m³/day, CGC Energía 2,704 m³/day in Austral onshore, and Petróleos Sudamericanos 2,628 m³/day. Together, these companies account for more than 85% of crude production, with the Neuquén Basin as the undisputed epicenter.

Behind each well is an army of contractors. Nabors Industries leads with rigs confirmed in Vaca Muerta, including the F-15 transferred from the Permian Basin, capable of 6,700-meter laterals.

San Antonio Internacional deployed walking rigs for YPF and Vista Energy, specialized in pad drilling. Weatherford and Schlumberger dominate hydraulic fracturing and cementing, while local firms — CYC, Harris, Unidad de Perforación and DLS — provide national units that reduce logistical costs and accelerate scaling without bottlenecks.

Geographic distribution: Neuquén 76%, San Jorge Gulf 24%

The basin-level distribution is telling: Neuquén recorded 478 productive wells (75.8% of the national total), reaching 681 total wells completed including nonproductive ones.

The San Jorge Gulf Basin added 153 wells (24.2%), led by PAE at Cerro Dragón, which operates more than 4,450 wells under secondary recovery. Activity in the Cuyana, Austral and Northwest basins was nearly nil, confirming the country’s dual structure of shale versus mature conventional plays.