War in the Middle East

JPMorgan does not typically title its market notes with statements in the present tense.

The Oil Flash Note from its Global Markets Strategy team carries a subtitle that leaves little room for interpretation: demand destruction has already begun. Not “could begin.” Not “is at risk.” It has already begun. The bank devotes the document to explaining why standard financial models are underestimating it.

The core argument hinges on a distinction that may seem technical but has direct market implications. There are two types of demand destruction. The first is what elasticity models capture: when prices rise enough, consumers adjust. The second occurs when physical inputs do not arrive regardless of the price buyers are willing to pay—what JPMorgan describes as demand destruction driven by the physical absence of inputs. That is what has been unfolding in Asia since mid-March, and it is what standard financial models fail to capture.

The bank’s arithmetic—and its limits

JPMorgan estimates in the Flash Note that the short-term price elasticity of global oil demand is –0.024. The figure is technical, but the implication is straightforward: it takes a roughly 40% increase above 12-month highs to reduce total consumption by just 1%. Translated into the current scenario, if Brent averaged $100 in March—it was trading around $110 at the start of March 20, according to Investing.com data—the price effect would cut about 1 million barrels per day (b/d) of global demand in April.

That is the floor of the adjustment projected by models. JPMorgan warns that this number does not account for two additional sources of destruction: losses from canceled flights in the Middle East and, above all, the direct physical shortage of refined products in Asia. Elasticity measures the response to price. It does not capture what happens when there is no product at the dock.

Variation by product is material, according to the Flash Note. Gasoline is the most elastic: petrochemical crackers can partially substitute it with ethane in cracking operations. Jet fuel shows intermediate elasticity—airlines cancel lightly booked flights as fuel costs rise. Fuel oil is the least elastic, as its demand comes from residential heating, maritime transport and power generation, uses with no immediate substitutes.

Asia in emergency mode: the map JPMorgan built

The second half of the Flash Note is an operator-by-operator inventory of shutdowns and cutbacks underway in Asia as of March 19. The level of detail is unusual for a markets strategy document and is itself a signal: JPMorgan deemed it necessary to document plant-by-plant disruptions to show clients this is not a future risk.

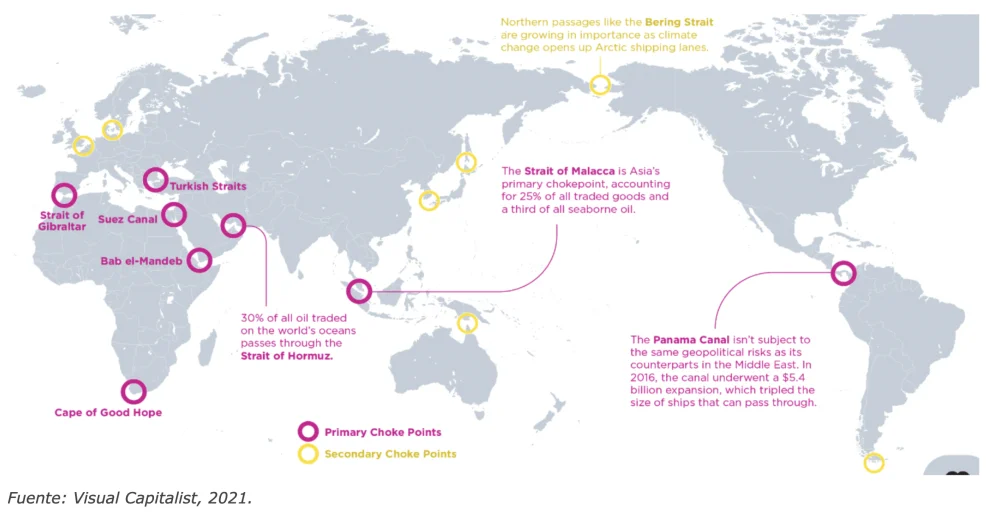

The petrochemical chain is the hardest hit. Ethylene crackers in Japan, South Korea, China, Indonesia and Taiwan source more than 50% of their naphtha from the Middle East, according to the note. With the Strait of Hormuz blocked since the start of the conflict on Feb. 28, that naphtha is not arriving.

In Japan, Mitsubishi Chemical and Mitsui Chemicals have cut ethylene output; Sumitomo Chemical may delay the restart of its Keiyo Ethylene plant. In South Korea, YNCC—one of the region’s largest ethylene producers, according to the bank—declared force majeure and is running crackers at reduced rates; Lotte Chemical and LG Chem warned they could follow. The South Korean government designated naphtha a strategic economic security item.

In China, Sinopec has reduced refinery runs by about 10% to preserve crude inventories. This comes alongside the shutdown of the ethylene cracker operated by the joint venture between Shell and CNOOC in Huizhou. Wanhua Chemical, for its part, declared force majeure for Middle East customers due to disruptions in liquefied petroleum gas (LPG) feedstock. In Indonesia, Chandra Asri is operating at reduced rates and declared force majeure after a sudden halt in feedstock arrivals. In Taiwan, Formosa Plastics Group’s Taiwan Petrochemical declared force majeure on March 10.

Aviation shows the same dynamic from another angle. With jet fuel near $200 per barrel, airlines have shifted from cost management to outright route cuts. As of March 18, according to the Flash Note, Qantas, Air India, Cathay Pacific and IndiGo had introduced tiered fuel surcharges. Air India imposed surcharges of between $125 and $200 per passenger on long-haul flights, with an additional $4.30 on domestic routes. Scandinavian Airlines and Air New Zealand were among the first to cancel or reduce flights outright.

Governments move into emergency mode

The response from Asian governments is, in JPMorgan’s view, further evidence that demand destruction has become an administrative phenomenon as well as a market-driven one. Bangladesh brought forward Eid al-Fitr and closed universities to save fuel. The Philippines and Sri Lanka introduced four-day workweeks. Pakistan shut schools and shifted universities to remote learning. Thailand and Vietnam encouraged work from home and limited vehicle use. Myanmar introduced alternating driving days. India suspended LPG shipments to commercial operators to prioritize household supply.

Taken together, these measures amount to what the Flash Note describes as emergency demand management—something standard price models do not anticipate because they do not incorporate direct state intervention in fuel markets.

The bias JPMorgan sees in prices

The document does not take the form of an explicit positioning recommendation—strategy flash notes rarely do—but the structure of the argument implies one. If standard elasticity underestimates real demand destruction because it fails to capture both the physical absence of inputs and emergency government intervention, then the models the market uses to project price adjustment are working with flawed assumptions.

Kpler estimated in a March 16 analysis that demand destruction in transport across Asia-Pacific could peak at 630,000 barrels per day in May—a figure that, because it is limited to transport, does not include industrial destruction from the lack of petrochemical feedstock.

Brent closed around $108 on March 19 after touching $119 in the same session. Intraday volatility reflects diplomatic signals the market processes in real time. What JPMorgan documents in its Flash Note is slower and deeper: demand destruction that has already begun, that models underestimate and that operates asymmetrically across products. Fuel oil does not give way because it lacks substitutes. Jet fuel falls along with the flights being canceled.